AI is No Longer an App: It’s a Tier 1 Infrastructure Shift

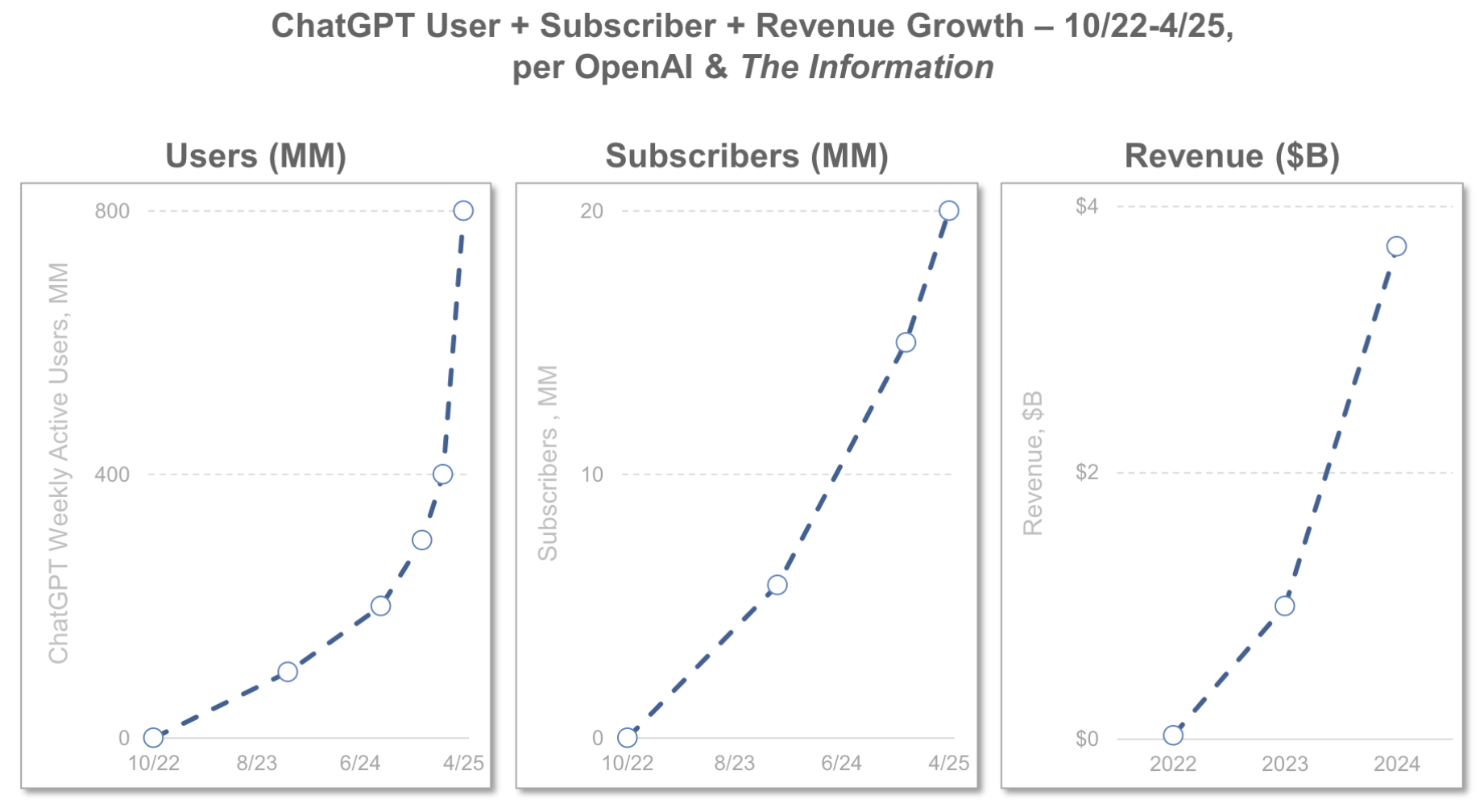

Forget ChatGPT’s user growth. The most dangerous number in Bond Capital’s 2025 AI report isn’t consumer adoption, it’s developer velocity.

NVIDIA’s developer base grew 6x to 6 million over seven years. Google’s Gemini developers grew 5x to 7 million in one year. This isn’t a tech trend; it’s a Tier 1 infrastructure explosion. When the “factories” are being built this fast, the window for “experimentation” has already closed.

From Tier 3 Toys to Tier 1 Tools

In my framework for Tier 1 Problems, I argue that most products fail because they solve “Nice-to-Have” (Tier 3) issues. For the last two years, Enterprise AI has mostly been Tier 3: chatbots that summarize meetings or write better emails.

The Bond Capital data shows the pivot to Tier 1—the “Must-Fix” problems:

- Carbon Robotics: AI-driven laserweeding has treated 230,000+ acres, replacing chemical glyphosate. This isn’t a “cool” feature; it’s a fundamental shift in agricultural economics.

- Waymo: Captured 27% of San Francisco’s rideshare market in just 20 months. That is the physical world being re-coded in real-time.

- Tesla: Replaced 330,000 lines of C++ code with neural networks.

These aren’t pilots. These are production systems solving the “bleeding” problems of labor scarcity and operational complexity.

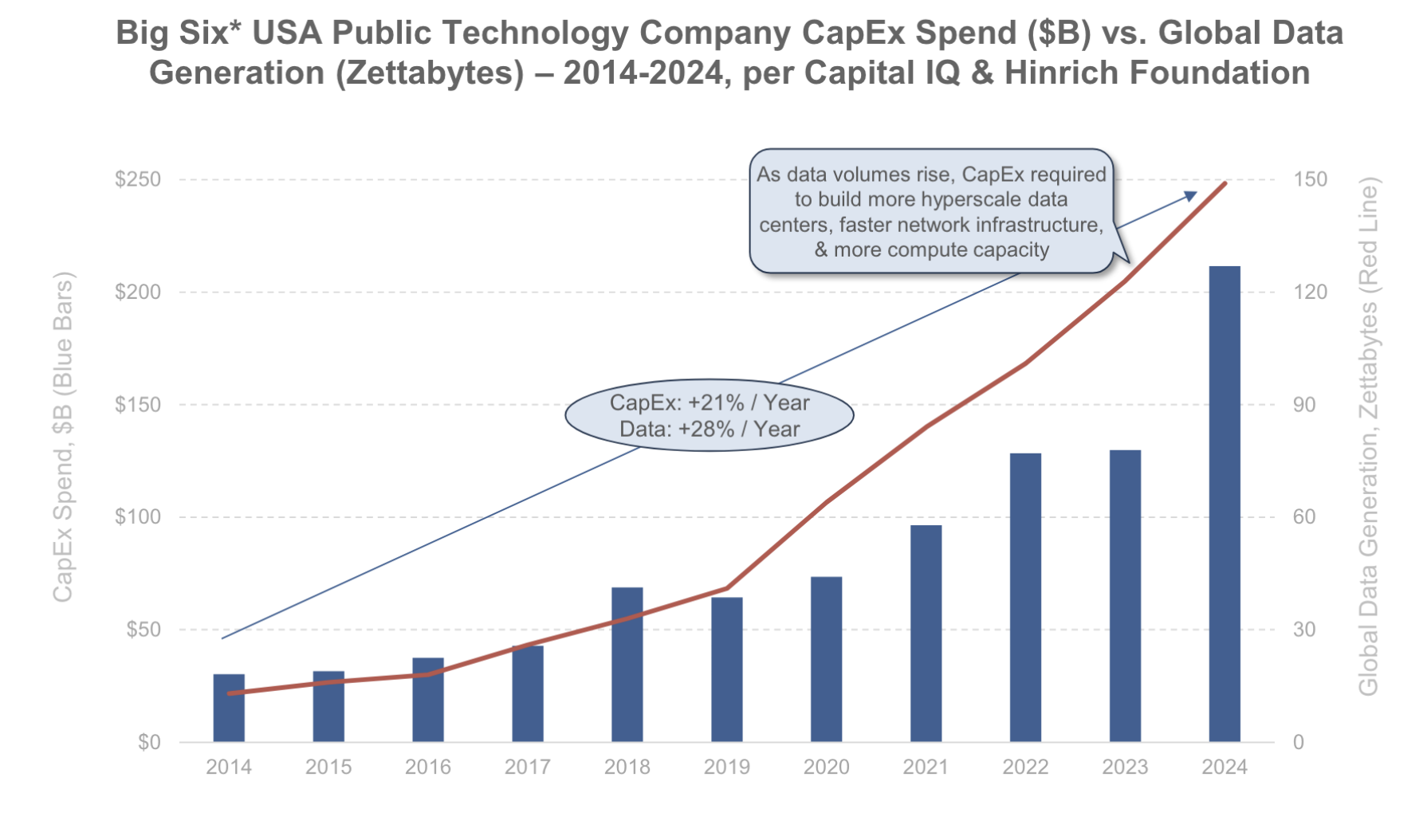

The “Factory” Economics

The Big Six (Apple, NVIDIA, Microsoft, Alphabet, Amazon, Meta) increased CapEx by 63% year-over-year. Amazon AWS’s CapEx as a percentage of revenue jumped from 4% in 2018 to 49% in 2024.

As NVIDIA CEO Jensen Huang puts it, these aren’t data centers; they are AI Factories. In the Tier 1 world, infrastructure is a “Must-Fix.” If you don’t own the compute or the integration, you are paying a “Tax” to those who do. Training costs are still high ($5B for OpenAI in 2024), but inference costs are plummeting. The “AI Tax” for switching providers is disappearing as model performance converges. The strategic question is no longer which AI to use, but how fast you can integrate it into your core “Must-Fix” workflows.

The Integration Window is Closing

The Bond Capital report highlights an uncomfortable truth: geographic competition is intensifying. China’s industrial robot installation has surged past the U.S., and apps like DeepSeek are gaining 54M users in months.

For the operator, the data points to three non-negotiable shifts:

Infrastructure over Applications: The money is flowing to the enablers (NVIDIA, TPU sales, AWS Trainium), not the generic “AI wrappers.”

Specialized over General: Success is found in solving known headaches in conservative industries (Mining, Ag-Tech, Logistics) rather than inventing new categories.

Speed as the Only Moat: The timeline compression is unprecedented. Electricity and the Internet took decades. AI is achieving the same penetration in months.

The Bottom Line

If your organization is still in the “AI Pilot” phase, you are solving a Tier 3 problem while your competitors are building Tier 1 factories.

Computational intelligence is becoming a commodity input, like electricity. In a world where intelligence is “free,” competitive advantage comes from operational excellence and integration speed. Stop watching the chatbots. Start watching the factories.